Decentralized Energy Based Currency

Decentralized Energy Based Currency

Inflation is rampant and a debt crisis looms. Meanwhile the energy economy is strangled. Perhaps there's a single solution to both?

Thermodynamics of Energy as a Currency

A few weeks ago I wrote a short essay exploring the concept of using energy as a means of backing currency, instead of the fiat currency the United States uses today which is backed by belief the US can repay its debts. At first it seemed like a fun thought experiment, but as I teased out the implications I was intrigued by how the physics of energy production and distribution could automatically solve some serious issues with fiat currency by aligning economic incentives along physical principles and preventing abuse of the monetary system. Here are those conclusions about an energy-backed currency in brief:

Inflation resistant. A government could not arbitrarily expand the money supply without also expanding its energy production, in contrast to a fiat monetary system in which additional debt can be issued without limit.

Optimizes for more production. In a capitalist economy investment dollars are always seeking the highest rate of return; in an energy-denominated currency this means activities that are energy producing or return-on-energy. Since energy is the number one most common factor of production across all goods and services it means we are incentivized to maximize the availability of the single most important factor of production.

Efficiency enforced by physical law. The natural tax on energy is entropy: everytime energy is produced, transmitted, or consumed some portion is lost as entropy. The constant tax of entropy incentivizes every business activity to be as physically efficient as possible, instead of optimizing for an arbitrary incentivized structure imposed by a regulatory framework like carbon credits, consumer rebates, etc, which can become co-opted by political interests beyond true efficiency.

Incentivizes grid resiliency: volatility in energy prices, bottlenecks in distribution or transmission, and idle generating capacity all represent arbitrage opportunities exploitable by businesses looking to earn energy-backed dollars.

Ultimately if we consider the capitalist industrial economy, like any organism or ecosystem, as something that is seeking to maximize the amount of free energy available to consume, and note that epochs in civilizational history are largely demarcated by the amount of available energy to make use of, it makes sense to choose energy availability as the ultimate reward function guiding economic development. Money isn’t actually a factor of production in the conventional sense, it can only be used to purchase factors of production. It is entirely possible for an economy to be generating positive returns as demarcated in fiat currency while having a declining amount of energy to make use of for its economic activities.

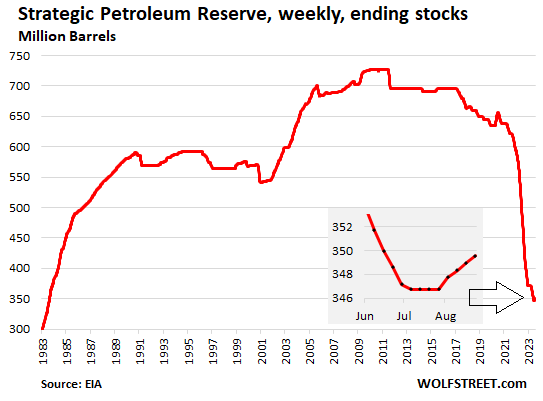

Of course, there are many areas where an energy-backed currency drastically departs from fiat currency, especially when it comes to monetary policy. Governments use central banks monetary policy to manage inflation, respond to economic crises, and push the economy through stable growth through the extension and contraction of credit to mitigate boom and bust cycles. In comparison, the closest analogue to a central bank in the energy economy is the Strategic Oil Reserve which can be drawn upon to smooth out fluctuations in gas and energy prices to insulate the economy from price shocks that would disrupt regular economic activity. Unlike the central bank, however, you can only draw down oil from the reserve if it actually has oil in the reserve. Energy is ultimately tied to a physical process that cannot be invented by the decision of a politician or unelected banker: you can only spend what you earn or save.

The issue today is that fiat currency has largely become a political tool for spending in the name of interest groups seeking economic benefit directly from the government. Excessive government spending has massively expanded the national debt, leading to drastic levels of inflation, and created countless perverse incentives in rent-seeking that generates monetary returns without delivering bottom-line value to society. When a government is able to spend money arbitrarily without regards to its revenues in taxation, and does so to capture political support to maintain its power, interest payment obligations to service the debt issued begins to surpass other major national spending areas like defense.

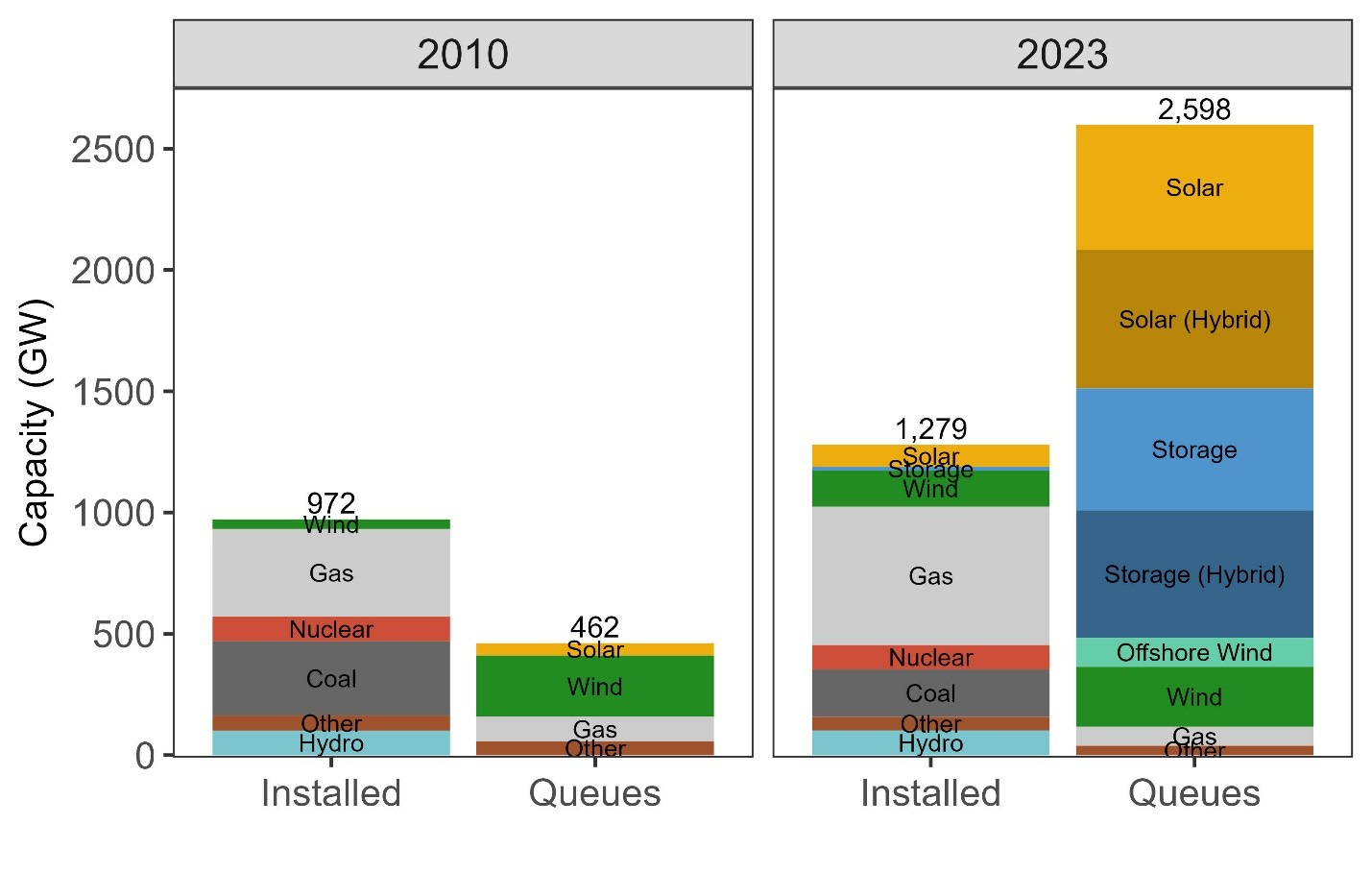

Governments are unlikely to surrender central banking anytime soon given the political leverage it grants, likewise the commercial sector is unlikely to support moving away from fractional-reserve banking thereby reducing its own ability to raise debt to finance future operations. However, there is a growing concern around devaluation of the US dollar due to government overspending among thinkers like Day Dalio, the rising national debt and its interest payments, widespread consumer inflation, and a regulatory environment around energy that makes it difficult to develop new infrastructure in both generating and transmission capacity: there is 1,200 GW of generating capacity in the US today, with another 1,500 GW in the interconnection queue awaiting approvals while approval time has grown from 2 years to 4 years in the last 6 years.

All this motivates answering the question in earnest, is it possible to produce a currency that is backed by energy, and how would it be executed? A currency that would naturally be resilient to inflation, limit government overspending, maximize producing the most important factors of production, and incentivize a robust energy infrastructure? After writing the original essay I came across the blockchain company Quai Network which is proposing to do exactly this, with a blockchain architecture ambitious enough to actually serve as a global system of currency useful for large volumes of transactions. Before digging into how a blockchain like Quai would work, let's first identify a few of the most common shortcomings of blockchain networks proposed as alternatives to fiat currency as well as dispel a common misconception that Bitcoin already is an ‘energy backed’ currency.

Limitations of Blockchain as a Currency

To effectively act as a currency while transactions are recorded on a distributed ledger like a blockchain, you need to handle a large volume of transactions per second, which naturally depends on how many transactions can be stored on a single block and how fast blocks are mined. A bitcoin block is fixed at 1MB, and the data required to record a transaction can take anywhere from 250 bytes to 1 kilobyte or more. The bitcoin protocol produces a new block every 10 minutes, meaning bitcoin can only record 3-7 transactions per second.

Despite being the de facto cryptocurrency of the world, bitcoin has been designed such that it is simply not usable as a currency for regular purchasing but rather acts as a store of value that is somewhat independent from other equities and currencies. In contrast, Ethereum doesn’t use a fixed block size in bytes but rather a fixed amount of ‘gas fees’ that correspond to each block, where gas fees represent the computational work required to execute operations or smart contracts. This decouples the amount of transactional work from the block mining rate by making the maximum gas fees per block something that miners can vote on as part of the protocol, increasing the effective transactions per block. The issue however is this: the current gas limit per block is around 30 million gas, and a simple ETH transfer takes 21,000 gas. Ethereum produces a new block every 12-14 seconds; if all transactions were simple transfers we have 110 transactions per second, however in practice many transactions are more complex than transfers meaning ethereum only supports 15-30 transactions per second.

The fact that the number one and number two most popular blockchain currencies are unusable as currencies has led to a large and complicated ecosystem of Layer 2 technologies, that seek to scale up the transaction processing volume and therefore usability of a base chain by producing what are in effect financial derivatives of the blockchain. In the regular economy this would be like if there was so little currency in circulation most people transacted in debt bonds that are ultimately settled in the underlying currency, when that currency became available. The issue is there become so many bonds in circulation issued by different entities it creates multiple disconnected ecosystems, with a bottleneck of reconciling those bonds in the underlying currency.

Isn’t Bitcoin already an energy-backed currency?

A common sentiment is that because the computational work involved in producing bitcoin or other proof-of-work currencies is extremely energy-intensive, bitcoin is already in practice an energy-backed currency. Let’s debunk this right away:

The embodied energy per bitcoin is not constant but depends on the overall volume of miners and the hardware they run. The difficulty of mining a block automatically adjusts to maintain an average 10-minute block issuance rate, meaning as more miners join the network the difficulty and therefore computational work and energy required increase; likewise as the hardware platforms evolve in mining bitcoin they also become more energy efficient. Therefore the energy required to produce any given block is constantly variable, and not directly tied to the number of bitcoin issued from the block as the reward per block also halves every 4 years.

While mining bitcoin does provide a way of generating revenue from under-utilized energy production, thereby defraying the cost of energy projects like solar and wind farms that suffer from mismatched demand and supply, bitcoin itself is not a currency pegged to a constant amount of energy like a kWh.

Scaling Energy-Backed Currency

Understanding the incentives behind an energy-backed currency and the limitations of the most popular blockchain currencies in actually handling large transaction volumes, we’re now in a position to see how Quai Network might actually deliver on an ‘energy coin’ usable at scale.

Proof of Entropy Minima vs Proof of Work

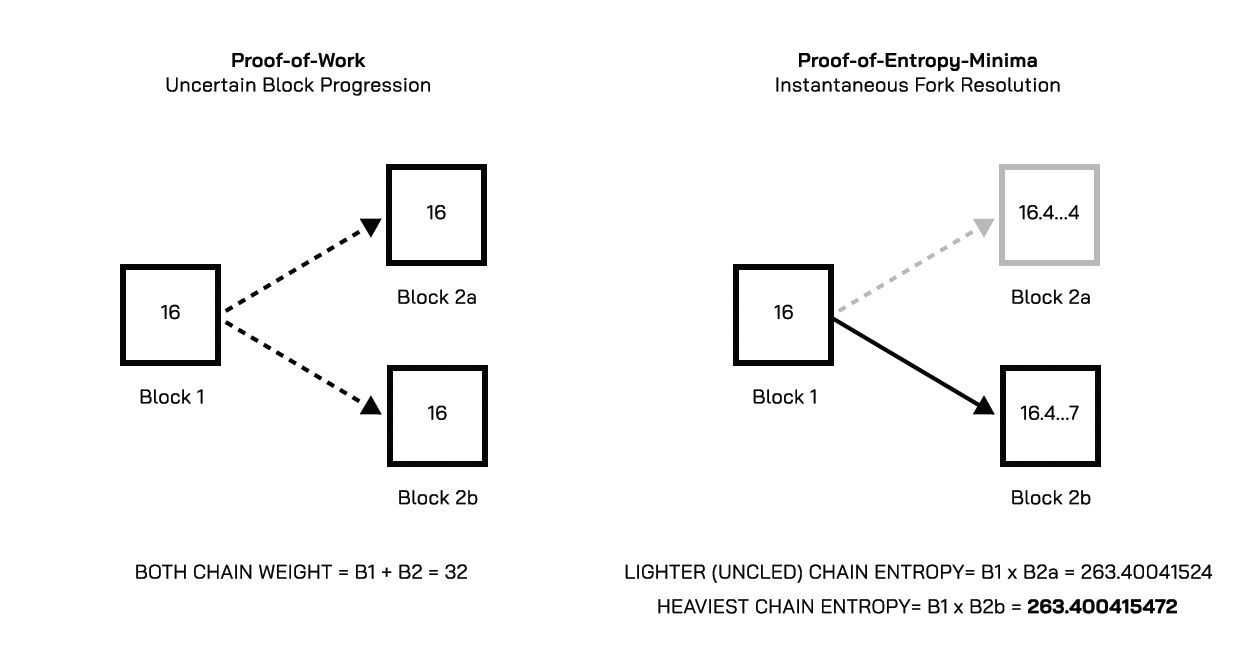

To produce a new block on a proof-of-work blockchain, miners have to solve a task of some computational difficulty that scales with the number of miners active on the chain such that the rate of producing new blocks stays relatively constant. For bitcoin the computational problem to be solved is this: take the header information of the previous block as well as a 32-bit number called a nonce, and run this through the Secure Hash Algorithm or SHA256 twice. This gets you a 32-byte number as an output, usually represented as a 64-character hexadecimal string. This number is the ‘answer’ to the computational proof-of-work problem, and the difficulty threshold basically says the number should be smaller than a certain amount for the miner who produced that solution to be rewarded with the next block on the chain.

As soon as a solution has been found that satisfies the difficulty level, this is broadcast to the network and miners take this new block as the starting point for looking for the next block. The issue with this approach is that the criteria for accepting a new block is simply that it is lower than the difficulty threshold - this means there are many possible solutions to the current computational problem. If two good-enough solutions are submitted at the same time, a fork is produced in the chain where miners work on both branches, and the network eventually converges onto whichever fork becomes the longest, leaving the other fork and the mining work embodied in it as an “orphan” and worth nothing.

We can frame this problem in the language of thermodynamics and information theory: considering the nonce value is permuted at random to try to find new lower-value hashes to the computational problem, a miner is essentially exploring a landscape of possible nonce configurations and looking for the value which produces the smallest resulting 32-bit number. Finding the subset of possible nonces that satisfy the difficulty threshold means reducing the total entropy of the solution, moving from any possible nonce value to the much smaller set of nonce values that give a valid solution. The only way to remove entropy from a system is by doing work and consuming energy - considering that any two nonce values that satisfy the difficulty threshold actually produce different 32-bit numbers, you can consider the lowest number as having removed the most entropy.

Quai Network uses the lowest-entropy sequence of blocks to resolve the forking and orphaning issues that plagues a simple difficulty threshold reward mechanism, by comparing the full 64-bit value of each hash and always choosing the one with the smallest value. This is why their Proof-of-Work method is something they call Proof of Entropy Minima.

Currency tied to the Cost of Electricity

Miners that find the next block in the chain, corresponding to the lowest-entropy solution, are rewarded with currency in proportion to the expected number of guesses used to find a solution of that specific entropy. This means the reward for each block isn’t constant like it is for bitcoin, but rather dynamically reflects the difficulty in mining that block. Also unlike bitcoin, the difficulty threshold is updated continuously for each block by using a look-back rolling period. If you make a reasonable estimate of the energy cost of each calculation used to produce an answer to the computational problem, have a reasonable estimate of the number of answers it took to find that solution, and scale the reward appropriately, Quai Network can issue currency in proportion to the energy it took to find that solution.

This simply isn’t feasible with bitcoin for the reasons mentioned above: the difficulty threshold doesn’t update continuously and there's a fixed reward of bitcoins per block that is actually decreasing over time. The embodied energy it takes to produce each bitcoin, assuming fixed hardware performance, goes up over time as more miners compete on the network for fewer and fewer issued coins.

Blockchain Currency to Scale

This all sounds well and good - a blockchain that avoids orphaned forks, and that rewards miners directly in proportion to the energy it took to mine a given block. If we could base economic activity on such a currency we effectively have a currency backed by energy - to produce more of the currency, we need to produce and consume more energy. There is no cheating by arbitrarily issuing new currency into circulation without first addressing the energy needs to produce said currency - limiting price distortions by reckless spending, avoiding runaway inflation, and naturally incentivizing removing bottlenecks or arbitrage opportunities in energy infrastructure to achieve a relatively flat and dependable cost of energy. Furthermore, the reward method itself can be adjusted over time to ensure that a coin issued a year from now represents the same amount of energy as a coin issued today.

The question is - how to scale a blockchain to actually handle the number of transactions per second necessary to run large amounts of economic activity? Recall that both bitcoin and ethereum support on average less than 20 transactions per second, relegating their effective use-case as either longer term stores of value or else an underlying asset upon which to build derivatives that must eventually be settled in that currency.

The solution pursued by Quai Network is in the technical weeds of blockchain implementation and is no longer directly tied to the thermodynamics of industrial capitalism or the follow-on benefits of a currency backed by energy, but they’re interesting to understand nonetheless.

Firstly, when mining bitcoin all the reward goes to whichever miner presents the first valid block - there's no fractional block rewards that someone gets for a half-way right answer. To distribute their individual risk, miners can join a pool that sets a lower difficulty threshold than required for the correct next block, whereby miners that meet this lower difficulty prove they are actively trying to contribute to the solution. If the pool succeeds in finding the next block, the reward is distributed proportionally to the number of lower difficulty guesses submitted by each miner instead of just to the miner who found the correct solution.

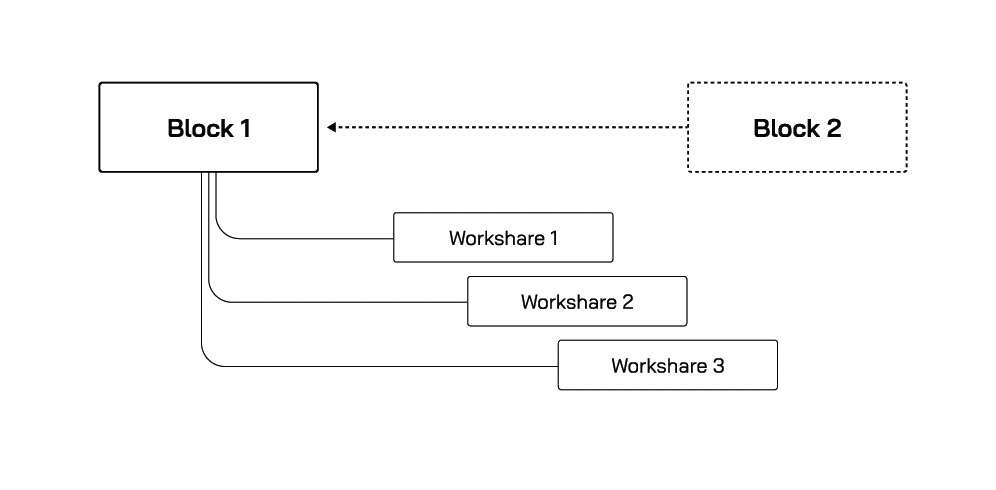

Quai incorporates this concept of mining pools intrinsically into the network with workshares, which represent attempts at solutions to the hashing problem that are not quite the right solution, but are signs of solutions attempted. Since transactions have to be stored in a block which takes time to produce, there is a lag between when a transaction can occur and when it is recorded. In bitcoin, this opens up the opportunity for a group of dedicated miners to flood the network with a large number of arbitrary transactions in a malicious attempt to disrupt the transaction recording process - a block with many transactions will propagate more slowly through the network, increasing the chances another miner can find a competing block before the solution has fully propagated, leading to a new fork and therefore ultimately a new orphaned branch.

To prevent this kind of malicious transaction-DDoS, Quai network records transactions into the history of workshares, ensuring that the transaction history is propagated throughout the network many times during the mining of each block, preventing transaction history from being discarded in an orphaned fork of the blockchain.

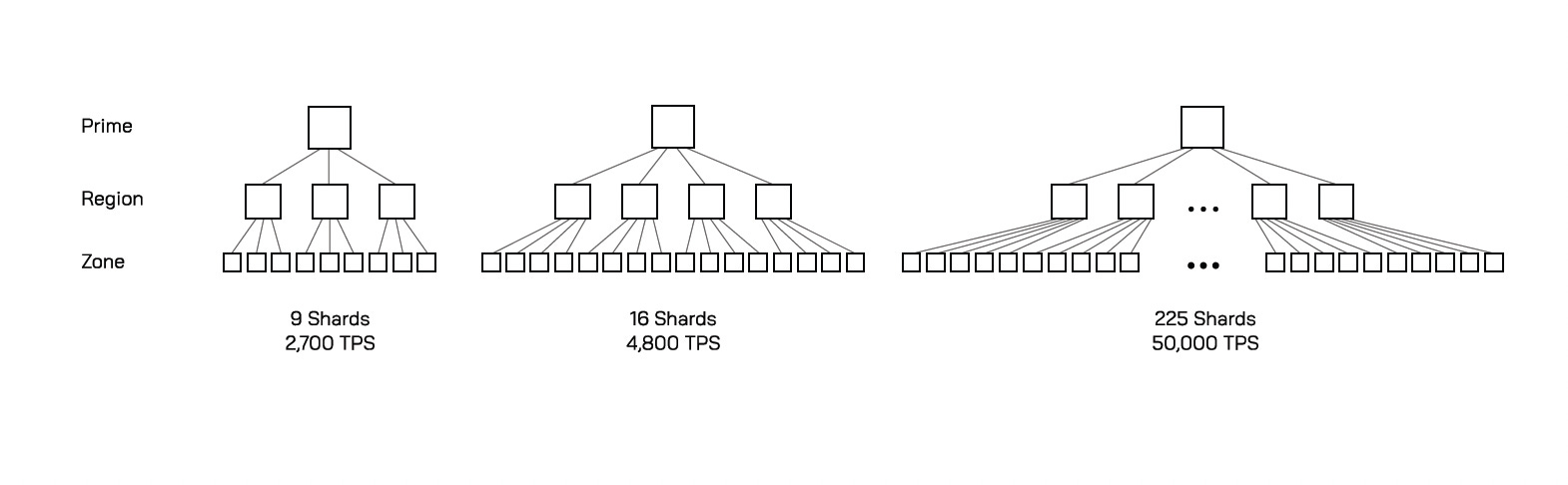

Recording transactions into workshares can help reduce the latency between when a transaction occurs when it's distributed to the entire network, and therefore permanently recorded, but how do you increase actual total transaction volume enough to satisfy the requirements of a functioning currency? The solution to this problem is the concept of sharding, which effectively splits the network into sub-units that can each operate in parallel by recognizing that transactions only ever involve just a few addresses, and so don’t need the attention of the entire network. If you split addresses up into groups and place each group in a shard, then transactions between addresses inside a single shard can be settled without needing to involve any other shard. Similarly, if a transaction involves addresses in two shards, then just those two shards are involved in recording the transaction while leaving other shares open to processing different transactions.

Splitting the network into shards like this can massively increase the total transaction processing throughput but there’s a catch - there’s an additional computational complexity in settling transactions across different shards, which reduces overall throughput, and so new shards are only created in response to growing network demand.

Thermodynamics of Industrial Capitalism

An energy-backed currency is a wholly different beast than fiat currency, but fiat currency itself is a departure from a previously established norm: to back currency with a country's gold reserves. The United States pursued a gold-backed currency in the aftermath of WW2 as part of the Bretton Woods system, which sought to establish stability in exchange rates between national currencies and promote economic growth and which established the price of gold as fixed at $35 USD per ounce. The issue however is that the US was unable to maintain enough gold reserves to completely back the amount of currency it issued - to do so it would have to constantly increase its gold holdings in proportion to the money supply. Gold is not something that can be mined arbitrarily like a digital currency produced by GPU’s in a server farm; you can’t just build a gold mine wherever you want.

Starting in the mid 1960s countries began to demand their gold deposits back from the US, leading to what in effect was a run on the Federal Reserve. In 1971 President Nixon was faced with a crisis - there was not enough gold reserves available to match the amount of US dollars held by foreign countries; when those countries demanded their gold back - including the French sending a battleship to the port of New York to collect its gold - Nixon did what he thought was necessary: he severed the $35 per ounce fixed rate of exchange between gold and the US dollar.

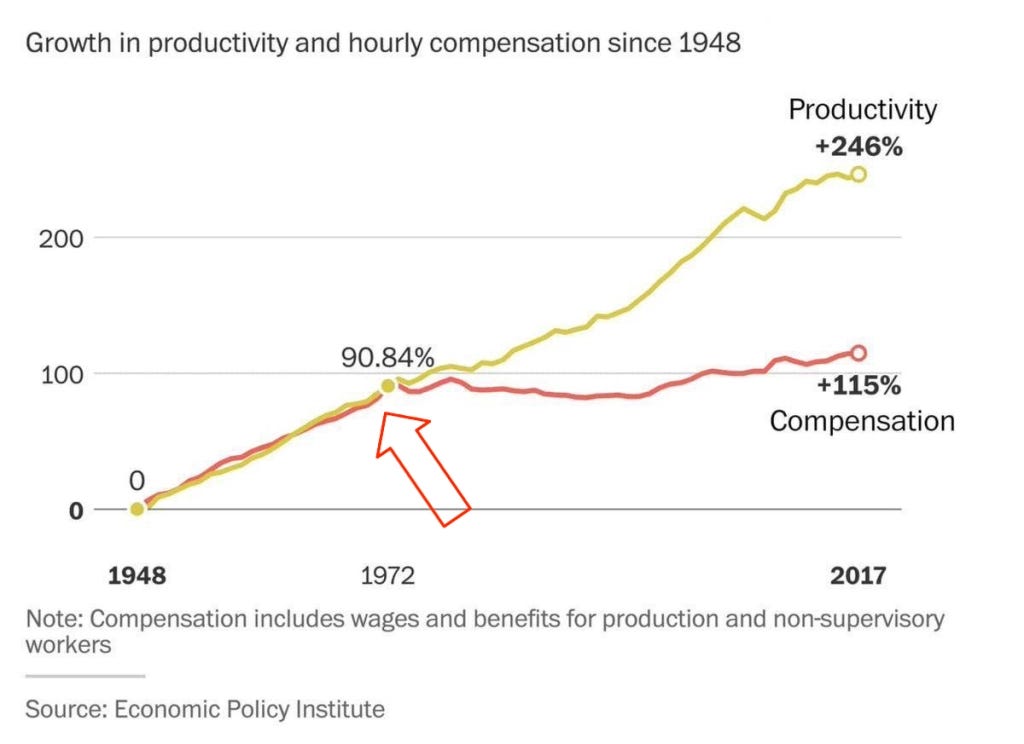

Ever since 1971 the United States has operated on a fiat currency, money backed by nothing but belief the US can repay its debts and supported by the inertia of the US dollar used as the de facto currency of international trade. Since then there has been no intrinsic limitation on the US Government’s ability to increase the money supply and issue new debt to finance its activities, and although the set of macro-economic circumstances since 1971 has been complex, an undeniable reality is that this year marked the divergence between growth in total GDP and real median weekly earnings leading many to wonder - what the hell happened in 1971?

The most immediate effect of Nixon's gold shock was inflation - the dollar became devalued relative to gold, and so the relative cost of foreign imports went up. The longer term effects are more difficult to tie directly to this one policy decision, but the simple fact is this: entering the era of fiat currency meant the government can expand its purchasing power arbitrarily, which distorts the effective functioning of markets by introducing politically motivated purchasing demand for certain goods and services, while the expanding money supply drives inflation which suppresses the signal implicit in returns-generating economic activity. If industrial capitalism is a thermodynamic process seeking to explore the configuration space of possible returns generating activity, the arbitrary expansion of the money supply effectively flattens the gradient. When money is close to free, i.e. when the interest rate set by the Federal Reserve is close to zero, there are less judicious investment decisions and large sums of cash are plowed into economically disastrous business ventures as was seen all throughout the ZIRP era.

To align the incentives of industrial capitalism we need to understand that money is ultimately the signal by which it navigates possible businesses and economic activities. If we want to maximize the economy’s ability to grow we need to maximize the production of the single most important factor of production, energy. An energy-backed currency has the potential to solve both these problems in one fell swoop, while also incentivizing as robust an energy production and distribution infrastructure as possible. Power to the people.

Truthfully, I did not read the full post yet, but you should research Lightning before commenting on Bitcoin transaction volumes. Much as the internet (and financial system) has layers, Bitcoin also has layers. Lightning is a Bitcoin "Layer 2" that has a theoretical unlimited transaction volume. Currently it is probably in the millions of transactions per second right now. Regrettfully it is the only "true" L2 right now, where "true" means using the native token. There are other L2s that use their own token and various sidechains. Ark protocol is a promising new idea being developed to be a true L2 using virtual UTXOs. For right now we have Lightning and it works very well but with some serious UX issues if you want to go self-custodial. As always... there's always tradeoffs.

Additionally, the argument that Bitcoin is not energy-backed because it's not a fixed amount of energy per bitcoin, falls flat. Yes, it is true that is is not fixed and there are very very good reasons for that. You don't want it fixed. Energy production is variable and you don't want the blockchain to get stuck in a bad state or gamed into a bad state. Regardless, if you look at a chart of Terahash / second (hashrate) it is EXPLODING up and to the right. Bitcoin uses a metric fuck ton of energy and that is a good thing because as you say we want to incentivize energy production for our civilization to progress.

I'm not sure Quai is but it is highly likely to supplant Bitcoin as the dominant cryptocurrency. Network effects are extremely important when it comes to money. I would argue that Bitcoin has already achieved escape velocity and everything that is being done on other chains will eventually come to Bitcoin if it is valuable enough / worth it to do so.

Anyways, I like your work and agree with your priorities to advance civilization. But, I think you need to go deeper on Bitcoin.